To quickly identify if a cost is a period cost or product cost, ask the question, “Is the cost directly or indirectly related to the production of products? Period costs are costs that cannot be capitalized on a company’s balance sheet. In other words, they are expensed in the period incurred and appear on the income statement. To make a profit and keep your bakery thriving, you’ll likely set a price for your cakes that’s higher than $10. Product costs help you set these prices, ensuring you cover all the expenses and have some left for profit.

This Smart Security Camera System Will Help You Keep An Eye On Your Home (And It’s On Sale For 62% Off Right Now)

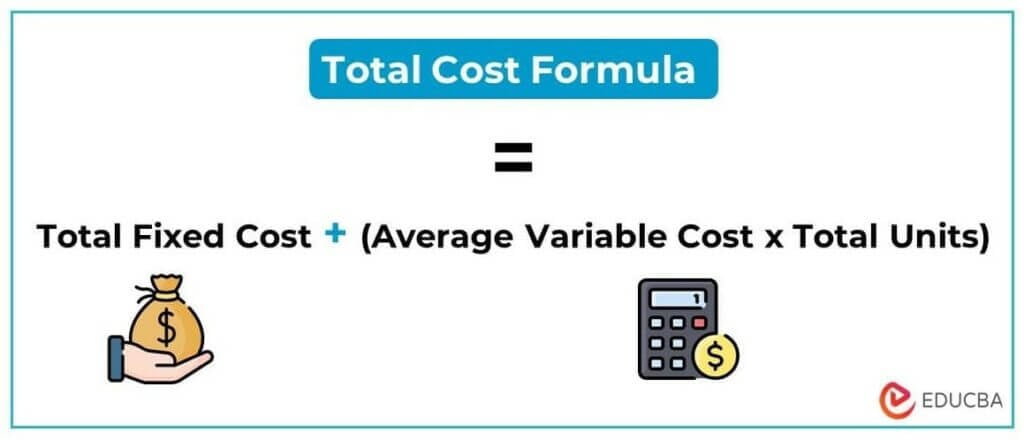

Manufacturing overhead costs include indirect materials, indirect labor, and all other manufacturing costs. If a product is unsold, the product costs will be reported as inventory on the balance sheet. When the product is sold, its cost is removed from inventory and will be included on the income statement as the cost of goods sold. Prime costs are the costs directly incurred to create a product or service. These costs are useful for determining the contribution margin of a product or service, as well as for calculating the absolute minimum price at which a product should be sold.

Product Costs

They occur consistently over a specific time period, like a month or a year, and are incurred regardless of how much or how little the business produces during that time. The difference between period costs vs product costs lies in traceability and allocability to the business’ main products and services. Easily traceable costs are product costs, but some product costs is rent a period cost require allocation since they can’t be traced. Otherwise, costs that can’t be traced or allocated to products and services are classified as period costs or costs that are attributed to the period in which they were incurred. If a manufacturer rents its manufacturing facilities and equipment, the rent is a product cost (as opposed to an expense of the period).

How much will you need each month during retirement?

Meanwhile, period costs are costs that are not related to production but are essential to the business as a whole. It’s important to distinguish between product vs period costs because the former must be deducted when a good or service is sold, whereas the latter is deducted in the period it is incurred. In summary, freight is a product cost if it is incurred as part of purchasing materials for manufacturing.

In other words, product costs are expenses that are initially “parked” in the balance sheet and recorded only as an expense (COGS) upon sale. Freight costs would be considered a product cost if the freight is to ship direct materials to the factory for production. For example, if a furniture manufacturer pays freight to transport lumber from a supplier to their factory, that freight cost gets included in the total cost to manufacture the furniture. Period costs are sometimes broken out into additional subcategories for selling activities and administrative activities.

Exploring Period Costs

If the related products are sold at once, then these costs are charged to the cost of goods sold immediately. If the products are not sold right away, then these costs are instead capitalized into the cost of inventory, and will be charged to expense later, when the products are eventually sold. Other examples of period costs include marketing expenses, rent (not directly tied to a production facility), office depreciation, and indirect labor. Also, interest expense on a company’s debt would be classified as a period cost. They are the costs that are directly and indirectly related to producing an item.

In managerial and cost accounting, period costs refer to costs that are not tied to or related to the production of inventory. Examples include selling, general and administrative (SG&A) expenses, marketing expenses, CEO salary, and rent expense relating to a corporate office. The costs are not related to the production of inventory and are therefore expensed in the period incurred. In short, all costs that are not involved in the production of a product (product costs) are period costs. These costs include direct materials, direct labor, and factory overhead.

- Product expenses are part of the cost of producing or acquiring an asset.

- Product costs are initially attached to product inventory and do not appear on income statement as expense until the product for which they have been incurred is sold and generates revenue for the business.

- Period costs are hard to pinpoint to the business’s main products, but they are incurred nonetheless because they’re essential.

Product costs help businesses figure out how much it truly costs to make each item they sell, helping set prices for profit. Period costs guide decisions on running the whole business efficiently, like deciding on staffing or advertising, ensuring everything works well financially. It’s like finding the right balance to make good products and keep the entire business in good shape. These are more like ongoing business expenses, not tied to a particular product but necessary for keeping the lights on. People often confuse product and period costs due to the complexity of accounting terminology and the different ways these costs are treated in financial reporting. One unique aspect of product costs is their treatment as assets until the product is sold.

If advertising happens in June, you will receive an invoice, and record the expense in June, even if you have terms that allow you to actually pay the expense in July. The cash may actually be spent on an item that will be incurred later, like insurance. It is important to understand through the accrual method of accounting, that expenses and income should be recognized when incurred, not necessarily when they are paid or cash received. If you manufacture a product, these costs would include direct materials and labor along with manufacturing overhead. Most of the components of a manufactured item will be raw materials that, when received, are recorded as inventory on the balance sheet. Only when they are used to produce and sell goods are they moved to cost of goods sold, which is located on the income statement.